Tax Refund Season 2026 Looks to Be a Big One: Here's Why

Get ready for a bigger tax refund this year! Learn why changes to tax laws mean more money back in your pocket. Find out how to file with confidence.

Tax refund season is officially underway, and early data suggests many filers could see larger checks this year.

According to the Internal Revenue Service (IRS), average refunds in early February were running about 11% higher than the same time last year — around $2,290 as of early filing data — though those numbers shift as more returns are processed.

What’s driving the increase? A combination of updated federal tax provisions, higher standard deductions, and refundable tax credits like the Earned Income Tax Credit (EITC) and the Additional Child Tax Credit. Together, these changes are reshaping what many households can expect back.

Tax law updates can feel overwhelming. That’s where we come in. At BenefitKarma, we track changes across government programs and break them down into simple, practical steps so you can file with confidence — and keep more of what you earn.

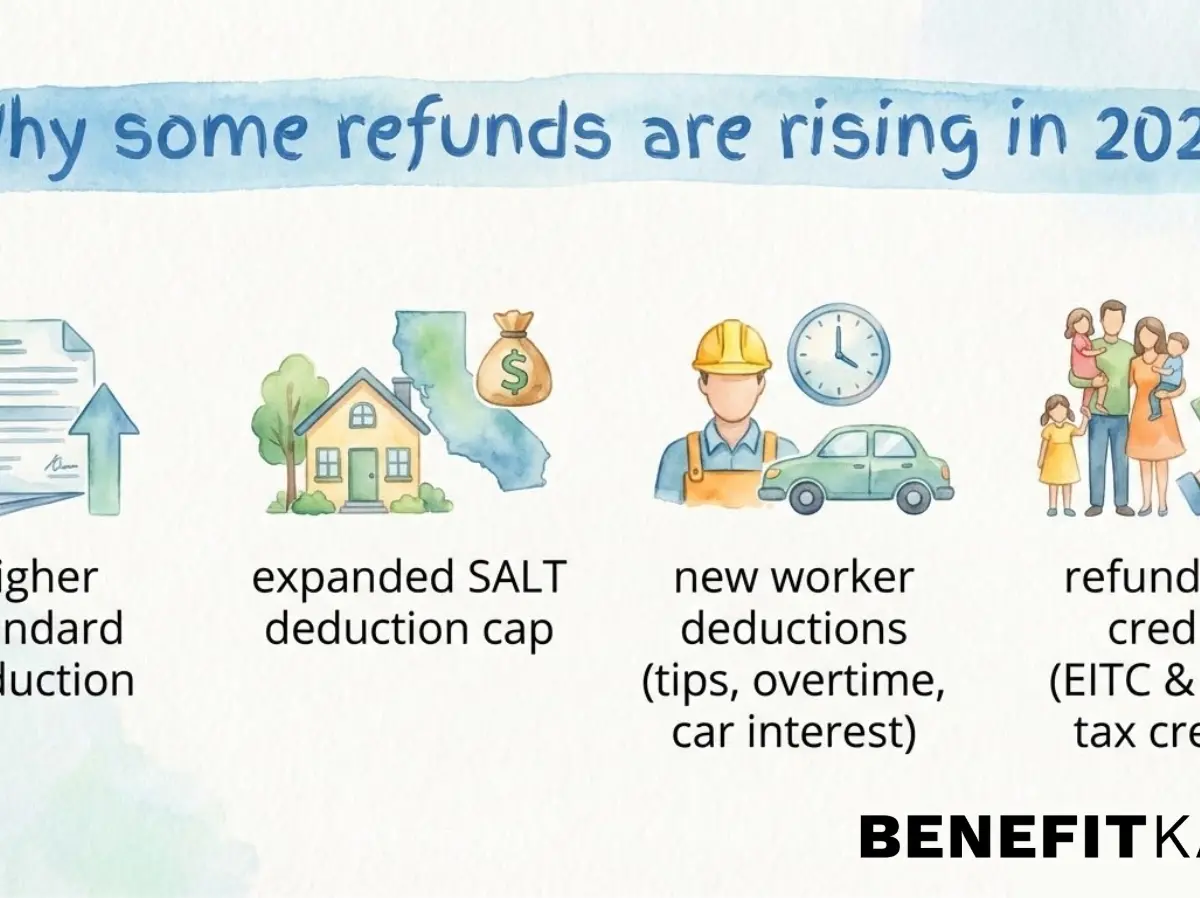

Why are refunds higher this year?

Refunds increase when one of three things happens:

- You paid more in taxes than you owed

- You qualify for new or larger deductions

- You qualify for refundable tax credits

Several recent federal updates are influencing 2026 refunds:

1. Higher standard deductions

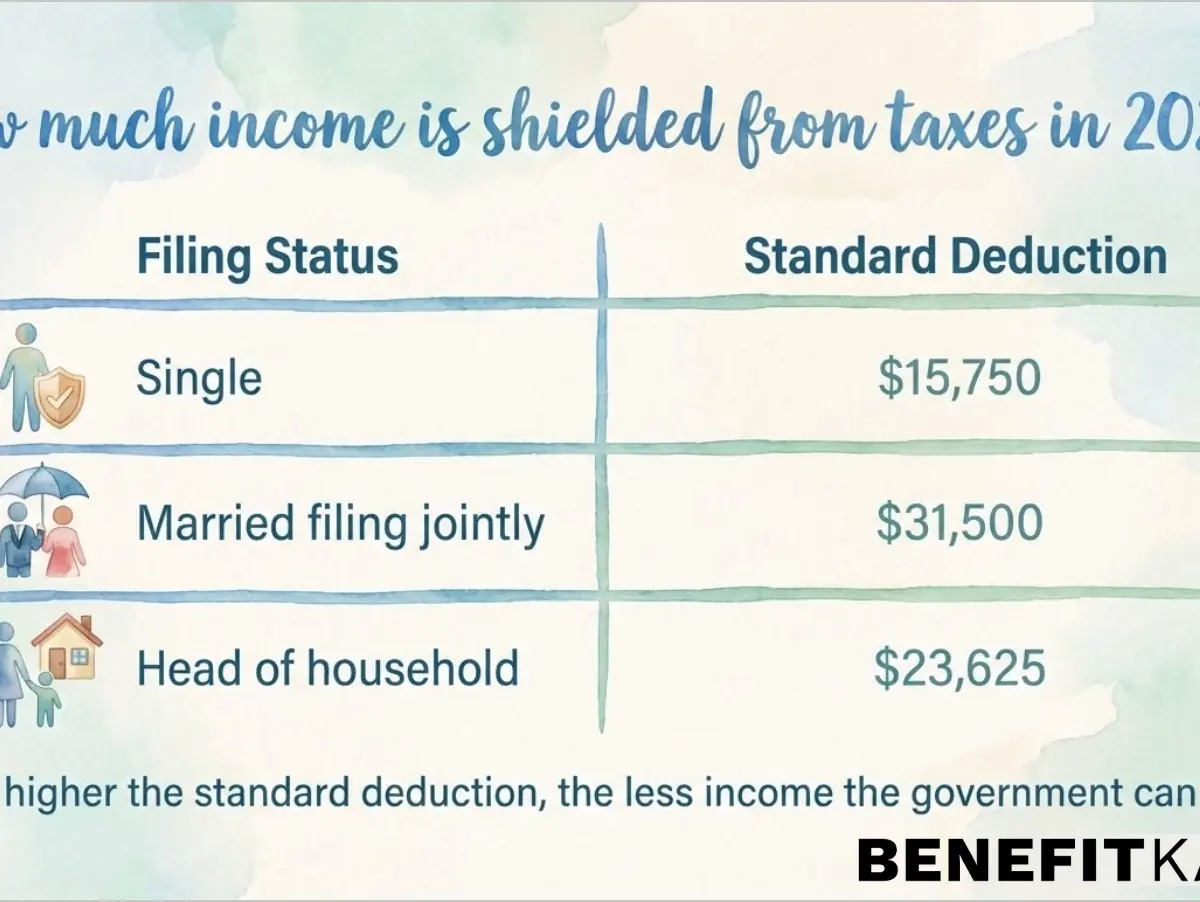

The standard deduction reduces the amount of income the government can tax. If you take the standard deduction (instead of itemizing), your taxable income drops automatically.

For 2026 filing season, standard deduction amounts have increased:

- Single filers: $15,750

- Married filing jointly: $31,500

- Head of household: $23,625

A higher standard deduction means more income is shielded from taxes — which can increase your refund if too much was withheld from your paycheck during the year.

2. Expanded SALT deduction cap

The State and Local Tax (SALT) deduction cap has increased from $10,000 to $40,000 for eligible filers. This matters most for people in higher-tax states like California, New York, and New Jersey.

If you itemize and paid:

- State income taxes

- Property taxes

- Local taxes

You may now be able to deduct more than in previous years. That reduces your taxable income — which can increase your refund or lower what you owe.

3. New deductions for certain workers

Recent federal tax updates also introduced or expanded deductions tied to:

- Qualified tips (up to annual limits)

- Certain overtime earnings

- Eligible car loan interest

- Additional deductions for people age 65 or older

A tax deduction lowers your taxable income. Less taxable income = less tax owed.

4. Refundable tax credits still matter most for working families

For low- and moderate-income households, refundable credits often have the biggest impact.

The Earned Income Tax Credit (EITC) is a refundable credit for working individuals and families with low to moderate income. “Refundable” means you can receive money back even if you owe little or no federal income tax.

The Additional Child Tax Credit works similarly for families with qualifying children.

These credits can add thousands of dollars to a refund, depending on income and family size.

What do the early IRS numbers show?

Try it: Find Benefits — Explore the full benefits library.

Last year, the IRS processed over 165 million individual returns, and about 94% were filed electronically.

Early 2026 filing data shows:

- Roughly 22.4 million returns received in the first 2+ weeks of filing

- Average refunds up about 11% compared to early last year

- Electronic filers typically receiving refunds within 21 days

Keep in mind: Early averages can fluctuate as more high-income and complex returns are filed later in the season.

Should you itemize or take the Standard Deduction?

Most taxpayers take the Standard Deduction. But you may benefit from itemizing if your total deductions exceed the standard amount.

Ask yourself:

- Did you pay significant mortgage interest?

- Did you pay high state or property taxes?

- Did you make charitable contributions?

- Did you have major medical expenses?

If those total more than your standard deduction, itemizing may increase your refund.

How to make sure you get the biggest refund you qualify for

Here’s a simple checklist:

- Review your W-2 and 1099 forms carefully: Make sure income and withholding match your records.

- Double-check eligibility for EITC and child credits: Many eligible families miss these every year.

- Compare standard deduction vs. itemizing: Run both scenarios if you’re unsure.

- File electronically: The IRS processes e-filed returns much faster.

- Consider professional help if your situation changed: Marriage, divorce, a new child, a home purchase, self-employment, or retirement can all affect your return.

A quick reality check about refunds

A bigger refund feels good — but remember what it means.

A tax refund is money you overpaid during the year. Ideally, you want your withholding to be close to your actual tax liability. A huge refund means you gave the government an interest-free loan.

If you consistently receive very large refunds, you may want to adjust your W-4 withholding so more money stays in your paycheck each month.

The bottom line

Tax refund season 2026 is shaping up to be stronger for many households thanks to updated deductions, expanded caps, and refundable credits. Early IRS data shows refunds running higher — but your personal outcome depends on your income, family size, deductions, and credits.

The key is knowing what applies to you.

At BenefitKarma, we stay on top of federal benefit updates, tax changes, and credit expansions so you don’t have to decode policy language on your own. Stay informed, file smart, and make sure you claim every dollar you qualify for.

Your refund is waiting — just make sure you’re ready for it.

Not sure what you qualify for?

A quick conversation can help you understand your options.

Optional — no obligation, fees may apply

Natural-sounding narration — pause, scrub, or speed up anytime.

Want help figuring out your next step?

Optional — fees may apply depending on your situation.

Some people choose to talk to a professional before taking their next step.

This might sound familiar:

You're not sure what to do next

You want someone to walk through your options

The process feels overwhelming

If that sounds like you, this might be worth a quick look.

Takes less than a minute

We only share your info with a service provider if you say yes.

Recommended Tools

Take action with our free tools

Get More from BenefitKarma

Create a free account to unlock all features

- Access premium benefit tools

- Personalized benefit matching

- Your personalized dashboard

Common questions about this guide

Frequently asked questions

Get more from BenefitKarma

Free tools, personalized dashboard & more