Parent PLUS Borrowers Face Higher Loan Payments

Parent PLUS borrowers may soon face higher loan payments. Learn what changes are coming and how to protect your budget.

Concerned rumblings among consumer advocates point to a tightening cash flow scenario for parents who took out student loans to fund their child’s education. The financial concern centers on major changes to the federal Parent PLUS loan program under the recently passed One Big Beautiful Bill Act.

If parents don’t take action soon, they could lose access to income-driven repayment (IDR) plans and certain loan forgiveness pathways. That means higher monthly payments, longer repayment timelines, and more interest paid over time.

Let’s break down what’s happening, why it matters, and what you can do right now to protect your budget.

Why are Parent PLUS borrowers at risk?

Under the One Big Beautiful Bill Act, Parent PLUS borrowers are set to lose eligibility for Income-Driven Repayment (IDR) plans beginning in July 2026.

Today, some Parent PLUS borrowers can access IDR plans after consolidating into a Direct Consolidation Loan. IDR plans cap monthly payments based on a percentage of discretionary income and can lead to loan forgiveness after a set number of years.

As of recent federal data from the U.S. Department of Education, roughly 3.6 million Americans hold Parent PLUS loans, with total balances exceeding $116 billion. The average parent borrower owes about $32,000.

For many families, IDR has been the only affordable way to manage those payments — especially for parents nearing retirement.

If IDR access is removed, borrowers will default to more rigid repayment structures that do not adjust based on income. For parents on fixed incomes or approaching retirement, that could mean serious financial strain.

[object Object],[object Object],[object Object]

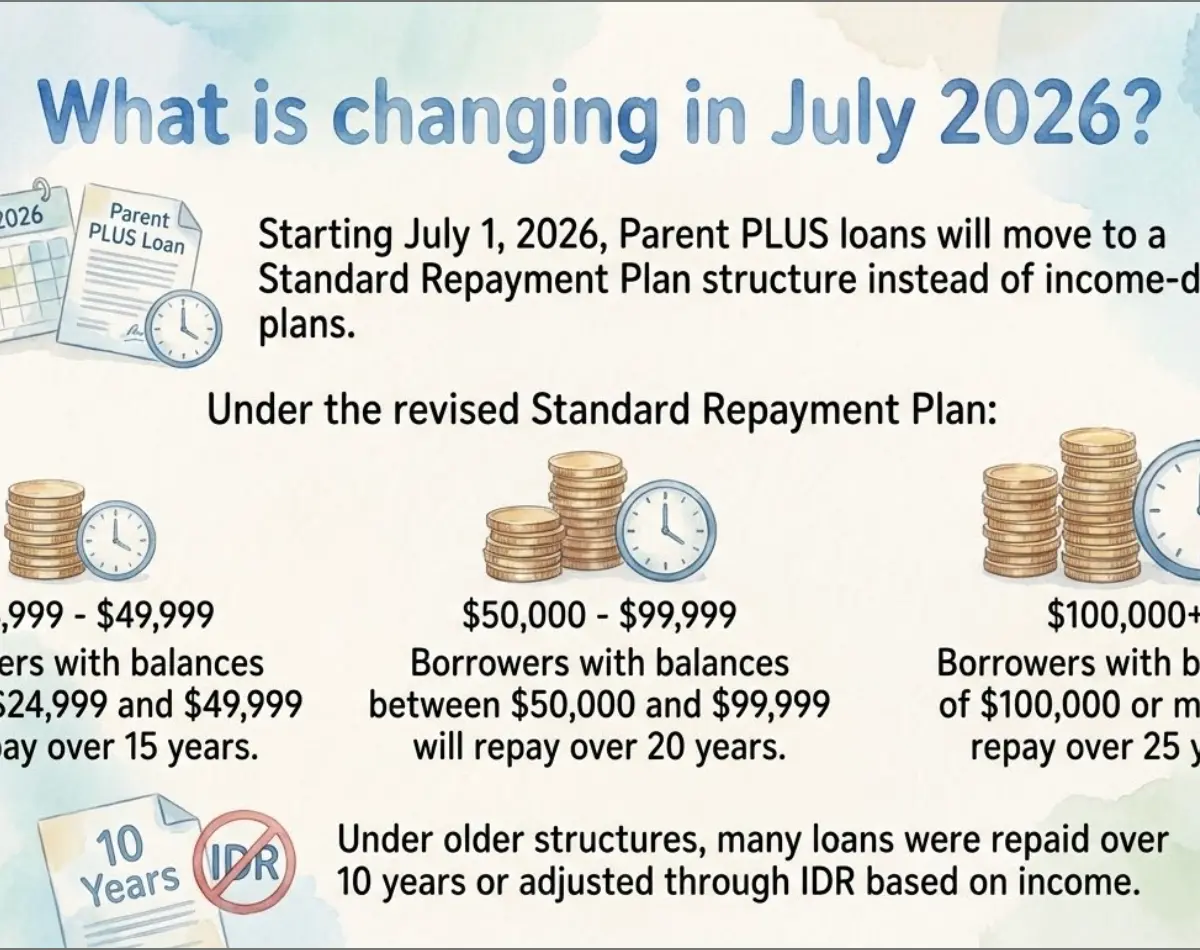

What is changing in July 2026?

Try it: Find Benefits — Explore the full benefits library.

Starting July 1, 2026, Parent PLUS loans will move to a Standard Repayment Plan structure instead of income-driven plans.

Under the revised Standard Repayment Plan:

- Borrowers with balances between $24,999 and $49,999 will repay over 15 years

- Borrowers with balances between $50,000 and $99,999 will repay over 20 years

- Borrowers with balances of $100,000 or more will repay over 25 years

Under older structures, many loans were repaid over 10 years or adjusted through IDR based on income.

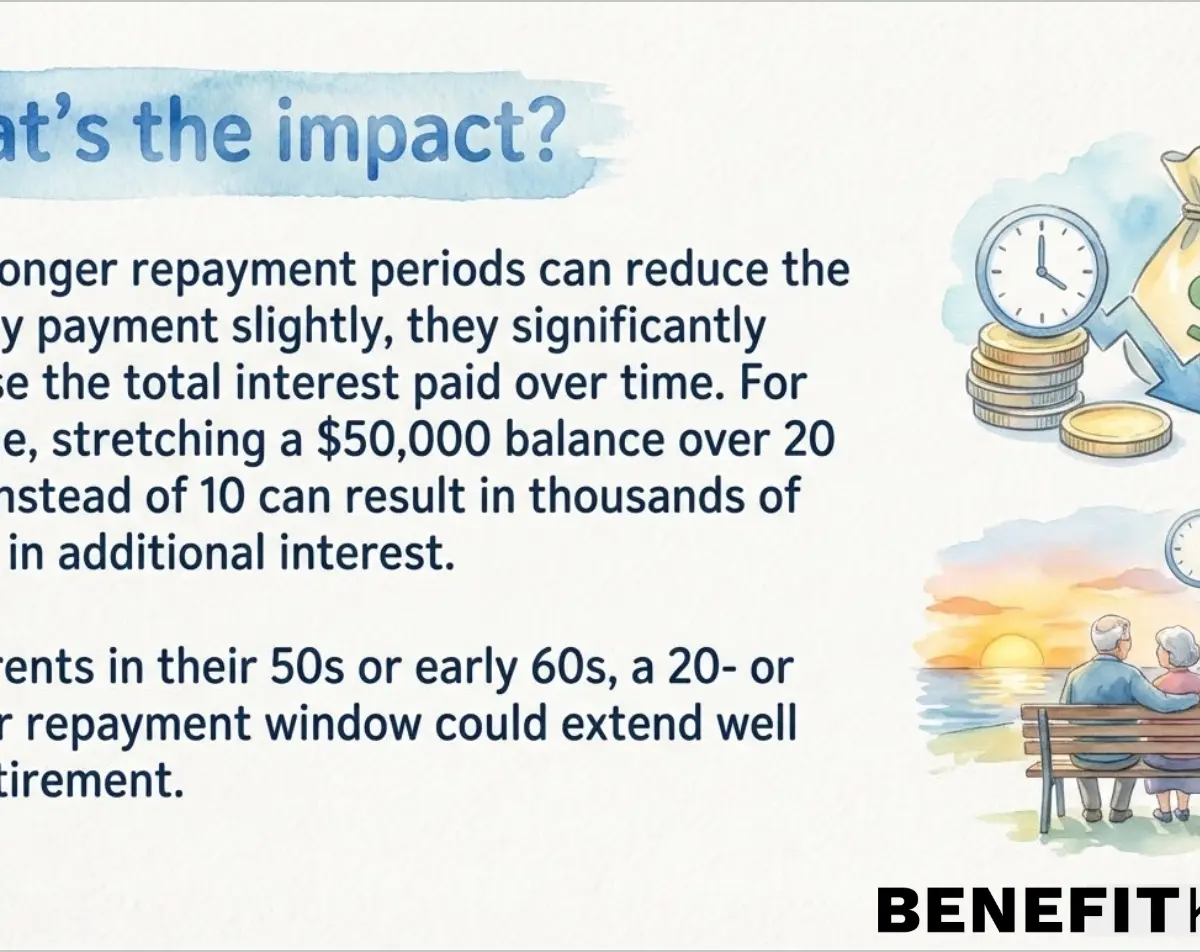

While longer repayment periods can reduce the monthly payment slightly, they significantly increase the total interest paid over time. For example, stretching a $50,000 balance over 20 years instead of 10 can result in thousands of dollars in additional interest.

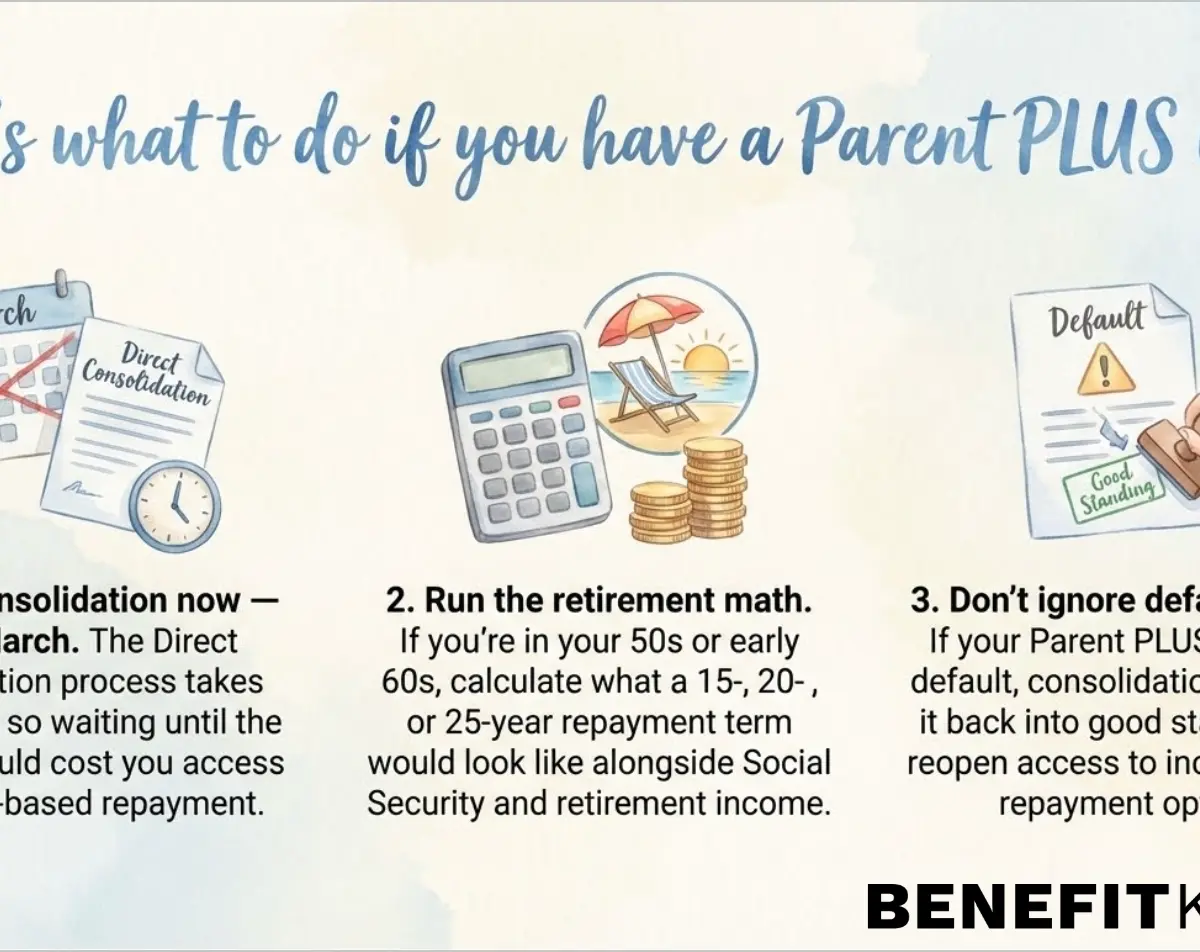

For parents in their 50s or early 60s, a 20- or 25-year repayment window could extend well into retirement.

Why this matters for retirement planning

Parent PLUS loans are unique because they are taken out by parents, not students. That means the responsibility remains with the borrower — even if the student struggles financially.

Unlike student borrowers who may be early in their careers, many Parent PLUS borrowers are:

- Within 10–15 years of retirement

- Managing mortgages or healthcare costs

- Helping multiple children with education expenses

A fixed repayment plan that ignores income changes can disrupt long-term financial stability. Social Security income, retirement savings, and medical costs are rarely flexible. A student loan bill is.

Without income-based options, some borrowers may face higher risk of delinquency or default.

What can you do before the deadline?

There is still a narrow window to protect your repayment options.

Before the new rules fully take effect, Parent PLUS borrowers can consolidate their loans into a Direct Consolidation Loan. This step is critical for maintaining access to the Income-Contingent Repayment (ICR) plan — currently the only income-driven option available to Parent PLUS borrowers after consolidation.

To preserve these options, borrowers should:

- Apply for Direct Loan consolidation before March 31, 2026

- Enroll in the Income-Contingent Repayment (ICR) plan

- Make at least one qualifying payment under ICR

After meeting these requirements, some borrowers may be able to transition into other income-based options, depending on eligibility rules in place at that time.

The consolidation process typically takes 4-6 weeks, so waiting until the last minute could jeopardize eligibility.

If your loan is already in default, consolidation can also bring it back into good standing and restore access to income-based repayment and forgiveness pathways.

How consolidation works (in simple terms)

Loan consolidation combines one or more federal student loans into a single new Direct Consolidation Loan.

The benefits may include:

- Access to certain repayment plans

- Simplified billing (one monthly payment)

- Resetting default status

However, consolidation may also capitalize unpaid interest, increasing your total balance. It’s important to review the long-term impact before proceeding.

You can apply through the Federal Student Aid website at StudentAid.gov, the official portal of the U.S. Department of Education.

Should everyone consolidate?

Not necessarily.

Consolidation makes the most sense for Parent PLUS borrowers who:

- Need lower monthly payments

- Want access to income-driven repayment

- Are pursuing Public Service Loan Forgiveness (PSLF)

- Are currently in default

Borrowers who can comfortably afford their current payments and are close to payoff may not benefit.

Every financial situation is different, which is why acting early — and reviewing your options carefully — matters.

The bottom line

Policy changes can feel overwhelming, but they also create opportunities for smart planning.

For Parent PLUS borrowers, the upcoming shift away from income-driven repayment could significantly increase monthly obligations and extend repayment well into retirement. With more than $116 billion in Parent PLUS debt nationwide, the stakes are high.

The key takeaway: Act before March 31 if consolidation makes sense for you. Waiting could permanently close the door on more affordable repayment options.

BenefitKarma is here to help you stay informed about changes to federal student loans, Social Security, disability benefits, and other essential programs. When policies shift, knowing your options is the first step toward protecting your financial future.

Not sure what you qualify for?

A quick conversation can help you understand your options.

Optional — no obligation, fees may apply

Natural-sounding narration — pause, scrub, or speed up anytime.

Want help figuring out your next step?

Optional — fees may apply depending on your situation.

Some people choose to talk to a professional before taking their next step.

This might sound familiar:

You're not sure what to do next

You want someone to walk through your options

The process feels overwhelming

If that sounds like you, this might be worth a quick look.

Takes less than a minute

We only share your info with a service provider if you say yes.

Recommended Tools

Take action with our free tools

Get More from BenefitKarma

Create a free account to unlock all features

- Access premium benefit tools

- Personalized benefit matching

- Your personalized dashboard

Common questions about this guide

Frequently asked questions

Get more from BenefitKarma

Free tools, personalized dashboard & more