# BenefitKarma — Full Content Dump (llms-full.txt)

> Companion to https://benefitkarma.com/llms.txt. Contains the full body of every published article, every glossary definition, and every state resource. Intended for AI ingestion with sufficient context window.

Generated: 2026-07-07

Source of truth: https://benefitkarma.com

Counts: 247 articles · 340 glossary terms · 51 state resources

All content is for educational purposes. BenefitKarma is not a government agency. Tool outputs are estimates only. Verify final eligibility and amounts with the relevant agency.

========================================

# Articles (247)

========================================

---

type: article

title: Understanding the 5 Million Drop in Medicaid and ACA Enrollment

url: https://benefitkarma.com/articles/health-disability/5-million-drop-in-medicaid-and-aca-enrollment

updated: 2026-07-01

---

# Understanding the 5 Million Drop in Medicaid and ACA Enrollment

More than 5 million fewer people are enrolled in Medicaid, CHIP, or Affordable Care Act marketplace plans than last year. For families who depend on these programs for doctor visits, prescriptions, hospital care, mental health treatment, and children's coverage, that's a serious warning sign.

The drop traces to two major changes: new Medicaid rules in the 2025 federal budget law and the expiration of enhanced ACA subsidies that helped millions afford monthly premiums. Many of these changes are still taking effect, so more people could be affected in the months ahead.

BenefitKarma can help you keep track of what benefits you may qualify for. Stay informed and take control of your coverage.

### Why did enrollment drop?

For ACA marketplace plans, cost is the main driver. When enhanced premium tax credits expired, many people saw their monthly premiums spike. Some switched to cheaper plans with higher deductibles. Others dropped coverage entirely.

For Medicaid and CHIP, the picture is more complicated. Medicaid eligibility is based on income, household size, age, disability status, pregnancy, and state rules — but people can lose coverage even when they still qualify if they miss renewal paperwork or can't complete a new requirement on time.

The 2025 federal budget law added new Medicaid work reporting requirements, more frequent eligibility checks, and new limits on how states fund their programs. Many of these rules are just beginning to roll out.

### Who is most affected?

Those most likely to feel these changes include adults in Medicaid expansion, people who buy ACA coverage independently, self-employed and gig workers, parents using CHIP, and people with low or fluctuating income. Immigrants and mixed-status families may also be avoiding enrollment due to concerns about immigration enforcement — a dynamic researchers call a "chilling effect."

Some states have seen especially sharp drops. Medicaid and CHIP declines have been most pronounced in Indiana, Louisiana, Arizona, Rhode Island, and Delaware. ACA drops have been steepest in North Carolina, Ohio, West Virginia, Indiana, and Delaware.

Even if your state isn't on that list, watch your mail and online accounts. A missed notice can create a coverage gap.

### What about Medicaid work requirements?

This is the biggest policy change for many people. Some states — including Nebraska — have already implemented work requirements. Most states are expected to follow in January 2027.

Under these rules, certain adults must show they are working, in school, volunteering, or participating in job training for at least 80 hours per month. Exemptions may apply for people who are pregnant, medically frail, disabled, or caring for certain family members, but exact rules vary by state.

The requirement isn't just about whether you work — it's about whether you can prove it the way your state requires. Paperwork, deadlines, and online forms matter.

### Can children lose coverage too?

Yes. Children aren't the target of work requirements, but they can lose coverage if a household misses renewal paperwork or if state systems create new barriers. Parents should watch for renewal notices even if their child has been covered for years.

If your child loses Medicaid or CHIP, options remain. CHIP has different income limits, and some children qualify even when parents don't. Losing Medicaid or CHIP also typically triggers a Special Enrollment Period for ACA marketplace coverage.

### What should I do if I lost coverage?

If you lost Medicaid or CHIP: Find out why. If it was a paperwork issue, you may be able to reopen your case by submitting the missing information. If your income is now too high, check whether you qualify for an ACA plan. Ask whether your children still qualify for CHIP — income limits for children are often higher than for adults.

If your ACA plan got too expensive: Don't assume you have no options. Log in and compare plans — a different metal level or insurer may lower your payment. Update your income estimate if your situation changed. If you recently lost job-based coverage, had a baby, moved, or experienced another major life change, you may qualify for a Special Enrollment Period.

### How do I protect my coverage?

Make sure your Medicaid office or marketplace has your current address, email, and phone number. Open every notice, even routine-looking ones. Check your online account monthly. Save pay stubs, school records, volunteer documentation, and medical paperwork that could help prove eligibility.

If you receive a notice you don't understand, don't wait — contact your state Medicaid office, ACA marketplace, a local navigator, legal aid, or a community health center.

### Can I appeal if my coverage was ended?

Yes. If you believe your coverage ended in error, you have the right to appeal. Your notice should explain why coverage ended and how long you have to respond — deadlines can be short. In some Medicaid cases, you may be able to keep coverage during an appeal if you request it before the deadline, though rules vary by state.

### The bottom line

People are losing coverage because costs went up and rules are changing. But losing coverage doesn't always mean you're out of options. Check whether you qualify for Medicaid, CHIP, an ACA marketplace plan, or a Special Enrollment Period — and if you get a notice, respond quickly.

---

type: article

title: Help with Adopting: Understanding the Adoption Assistance Program

url: https://benefitkarma.com/articles/family-education/adoption-assistance-program-federal-subsidies

updated: 2026-07-01

---

# Help with Adopting: Understanding the Adoption Assistance Program

Adoption can be a beautiful way to grow your family — but it comes with real costs. The federal Adoption Assistance Program exists to help, offering monthly payments, Medicaid coverage, reimbursement for adoption expenses, and other support depending on the child's needs and your state's rules.

BenefitKarma can help you understand what benefits may be available. Visit BenefitKarma.com to learn more.

### What is the Adoption Assistance Program?

This program helps families adopt children — typically from foster care — who are considered to have "special needs" under state or federal rules. That term is broader than it sounds. A child may qualify due to age, medical or behavioral needs, disability, or being part of a sibling group.

The main federal version is called Title IV-E adoption assistance. Children who don't qualify federally may still qualify for state-funded assistance. Eligibility is based on the child's situation, not the adoptive family's income.

### What benefits can it provide?

Monthly payments. An adoption subsidy helps with ongoing costs like food, clothing, therapy, and child care. Amounts vary by state and child, and are usually negotiated before finalization — often capped at what the child would have received in foster care.

Medicaid. Many eligible children also receive Medicaid, covering doctor visits, prescriptions, mental health care, and other health needs. For children with trauma histories, developmental delays, or complex medical needs, this can be the most valuable benefit. Title IV-E Medicaid coverage generally continues even if your family moves to another state.

Non-recurring expense reimbursement. Families can often be reimbursed for one-time adoption costs — court fees, attorney fees, agency fees, and travel. Most states cap this at $2,000 per child. These must be approved before finalization, so keep all receipts.

State extras. Depending on where you live, additional support may include post-adoption counseling, respite care, support groups, or extended services for older youth.

### What about the federal adoption tax credit?

For tax year 2025, the maximum credit is $17,280 per eligible child. Up to $5,000 is refundable, meaning some families can receive part of it even if they don't owe that much in taxes. Qualified expenses include adoption fees, attorney fees, court costs, and travel.

The credit phases out for modified adjusted gross income above $259,190 and disappears above $299,190.

If you adopt a U.S. child determined to have special needs, you may be able to claim the full credit even if your out-of-pocket adoption costs were low — a significant benefit for families adopting from foster care.

### How do I apply?

Talk to your adoption worker as early as possible — ideally before finalization. Ask whether the child qualifies for adoption assistance, Medicaid, and nonrecurring expense reimbursement. Then make sure everything is documented in a signed adoption assistance agreement before the adoption is complete. Benefits approved after finalization are much harder to secure.

Before signing, get answers in writing to: the monthly payment amount, what Medicaid covers, whether benefits can be adjusted if needs change, how long benefits last, whether they continue past age 18, and what happens if you move states.

### The bottom line

Adoption assistance can make adoption more affordable and help families care for children with ongoing needs. The key is to ask early, understand what the child qualifies for, and get it in the agreement before the adoption is final.

---

type: article

title: Is Medicare Being Privatized? What A Proposed Enrollment Change Could Mean For You

url: https://benefitkarma.com/articles/benefits-in-the-news/is-medicare-being-privatized

updated: 2026-07-01

---

# Is Medicare Being Privatized? What A Proposed Enrollment Change Could Mean For You

Medicare is one of the most important health programs in the U.S., especially for older adults and people with disabilities. So when talk of major changes starts circulating, it's understandable to feel concerned — or even confused.

In March 2026, Trump Administration officials publicly confirmed they are exploring a major shift in how Americans are enrolled in Medicare. The proposal: automatically placing new beneficiaries into private Medicare Advantage plans instead of traditional government-run Medicare. It's a significant departure from how the system has worked for decades, and while nothing has been finalized, it raises important questions about cost, coverage, and control over your healthcare.

If you want clear, straightforward updates on benefits like Medicare, BenefitKarma is here to help you stay informed and make confident decisions.

## What's Actually Being Proposed

In March 2026, Chris Klomp, the Trump administration's director of Medicare, told reporters that the Centers for Medicare & Medicaid Services (CMS) is actively studying the feasibility of making Medicare Advantage (MA) the default enrollment option for new beneficiaries. No final decision has been made.

Currently, many people are automatically enrolled in traditional Medicare when they turn 65 if they are already receiving Social Security benefits — though automatic enrollment depends on specific conditions and doesn't apply to everyone.

Under the proposal being explored, new beneficiaries could instead be automatically placed into a private Medicare Advantage plan. They would still have the ability to switch or opt out, but the default — and what most people end up staying with — would change.

## Breaking Down Your Medicare Options

Try it: Find Benefits — Explore the full benefits library.

Understanding this proposal starts with knowing the difference between the two main types of Medicare:

### Traditional Medicare (Part A & Part B)

- Covers hospital care (Part A) and outpatient/doctor services (Part B)

- Run directly by the federal government

- Lets you see most doctors nationwide who accept Medicare

- Does not usually include dental, vision, or prescription drug coverage

### Medicare Advantage (Part C)

- Offered by private insurance companies

- Includes Parts A and B, often with extras like dental, vision, and drug coverage

- Requires you to use a network of providers

- May have lower upfront costs but more restrictions

The key trade-off: flexibility vs. bundled benefits.

## Why Some Experts Are Concerned

Critics argue that shifting default enrollment to Medicare Advantage could lead to higher costs and more restrictions over time.

One major concern is overpayments to Medicare Advantage plans. The Medicare Payment Advisory Commission (MedPAC) has estimated tens of billions in annual overpayments, and projections from the Committee for a Responsible Federal Budget suggest this could total at least $1.2 trillion over the next decade, with updated estimates trending even higher.

These overpayments can affect everyone, not just those enrolled in Medicare Advantage. The Joint Economic Committee found that in 2025, these excess payments increased Medicare Part B premiums by about $212 per enrollee, totaling billions in higher costs across the program.

There are also concerns about access to care. Because Medicare Advantage plans use provider networks, patients may have fewer choices compared to traditional Medicare, and some services may require prior authorization.

## A Risk Many People Don’t Realize: Medigap Access

One of the most important (and often overlooked) issues is how this shift could affect access to Medigap supplemental insurance.

Medigap plans help cover out-of-pocket costs in traditional Medicare. But in most states, you only have a guaranteed right to buy a Medigap plan when you first enroll in Medicare.

If someone is automatically enrolled in Medicare Advantage and later decides to switch back to traditional Medicare, they may not be guaranteed access to a Medigap plan.

That could leave them with higher out-of-pocket costs or fewer coverage options.

This is a key concern for critics and an important factor to consider when comparing plans.

## Is This Really “Privatization”?

The idea of “privatizing Medicare” is debated, and the answer depends on how you define it.

Medicare Advantage has existed for decades, and more than half of Medicare beneficiaries already choose these plans voluntarily. What’s being discussed now isn’t the introduction of private plans, but a change in the default enrollment system.

That distinction matters. Default choices can strongly influence what people end up using, even if other options remain available.

## Why Others Support The Shift

Supporters of Medicare Advantage point to its convenience and additional benefits. Many plans include:

- Prescription drug coverage

- Dental and vision care

- Wellness programs

For some people, especially those looking for all-in-one coverage, these plans can be appealing and easier to manage.

## What Could Happen Next

Right now, this proposal is still in the early stages and hasn’t been finalized, but there is a clear path it would likely follow if it moves forward.

First, federal officials would need to decide how to implement the change. That could happen through a formal rulemaking process, where details are published publicly and open for comment, or through a smaller pilot program to test how default enrollment into Medicare Advantage would work in practice.

Either way, the proposal would face significant scrutiny from lawmakers, advocacy groups, and the healthcare industry.

There’s also an open question about whether this kind of change can be made administratively or if it would require approval from Congress. That alone could slow things down or reshape the proposal entirely.

Even in a best-case scenario, changes like this take time. If the idea gains traction, the earliest meaningful shifts would likely happen over the next few years, not immediately. For now, the key takeaway is that this is a developing policy idea, not a finalized rule — but one worth paying close attention to as it evolves.

## What This Means For You

Even if this proposal moves forward, you would still likely have the option to switch plans or opt out of a default enrollment.

Still, defaults matter, and being informed ahead of time can make a big difference.

### Here’s what you can do now:

- Learn your options early before enrolling in Medicare

- Compare traditional Medicare and Medicare Advantage based on your needs

- Consider long-term factors like provider access and Medigap eligibility

- Stay updated on policy changes that could affect your coverage

## The Bottom Line

The idea of automatically enrolling people into Medicare Advantage instead of traditional Medicare could mark a meaningful shift in how the program works, but it wouldn’t eliminate your ability to choose.

The bigger issue is how that default might shape decisions, costs, and access to care over time.

BenefitKarma is here to break down complex benefit changes into simple, useful guidance so you can stay informed, ask the right questions, and make the best decision for your situation.

---

type: article

title: Is a Medicare Enrollment Freeze Coming for Hospice Providers?

url: https://benefitkarma.com/articles/benefits-in-the-news/medicare-enrollment-hospice-freeze

updated: 2026-05-13

---

# Is a Medicare Enrollment Freeze Coming for Hospice Providers?

For patients and families who rely on hospice care, and for the providers who deliver it, the idea of a federal enrollment freeze can sound alarming. But this isn't just a rumor anymore.

In late March 2026, a leading national hospice industry group formally called on the federal government to act, and the push is gaining real momentum. Here's what's actually happening, why it matters, and what you should do next.

BenefitKarma is here to translate complex policy developments into clear, actionable guidance so you're never caught off guard by changes that affect your care or your organization.

## What's Actually Being Proposed

On March 27, 2026, the National Partnership for Healthcare and Hospice Innovation (NPHI) sent a formal letter to CMS Administrator Dr. Mehmet Oz calling on the Centers for Medicare & Medicaid Services to implement a temporary, nationwide moratorium on new hospice provider enrollments, citing the continued growth of fraudulent providers exploiting the Medicare hospice benefit.

A moratorium would temporarily halt new hospice providers from enrolling in Medicare — essentially freezing the front door to the program while regulators work to clean up what's already inside. No moratorium has been officially implemented for hospice as of April 2026, but the call from a major industry organization — not a fringe group, but one representing leading nonprofit hospice providers — marks a significant escalation from rumor to formal policy advocacy.

## Why This Is Happening Now

Try it: Find Benefits — Explore the full benefits library.

The Medicare hospice benefit has existed since 1982, providing comprehensive end-of-life care to patients with a terminal illness and a life expectancy of six months or less. It has long been a target for fraud, but the problem has worsened dramatically in recent years.

CMS in 2025 referred 343 cases to law enforcement for suspected fraud, representing $3.4 billion in fraudulent billing activity. Roughly 4,780 providers and service suppliers had their Medicare billing privileges revoked due to inappropriate behavior.

The fraud hotspots are concentrated geographically. Enhanced oversight in four states with elevated fraud risk — Arizona, California, Nevada, and Texas — has resulted in more than 200 hospice Medicare enrollment revocations for failure to comply with CMS requirements. CMS has since expanded this targeted oversight approach to additional states, including Georgia and Ohio.

The scale in California is particularly striking. According to the Washington Examiner, federal investigators have stripped billing privileges from three-fifths of newly enrolled hospice agencies that have continued to appear in California, and 35% of the remaining providers were flagged for corrective action.

In early April 2026, FBI agents executed arrest warrants across Southern California, charging 15 people in a $60 million Medicare hospice fraud scheme across nine separate investigations — a case federal prosecutors called "Operation Never Say Die."

## This Tool Has Been Used Before

CMS has used enrollment moratoria before for other provider types when fraud reaches a crisis point. Most recently, in February 2026, CMS imposed a six-month nationwide moratorium blocking new Medicare enrollments for certain medical supply companies, as part of its broader Comprehensive Regulations to Uncover Suspicious Healthcare (CRUSH) initiative. Hospice advocates are now pushing for similar action in their sector.

## What a Moratorium Would (and Wouldn't) Mean

It's important to understand what this kind of action actually does. Moratoria typically only affect new enrollment applications. Existing enrolled providers continue operating normally and are not subject to the freeze. If you or a loved one is currently receiving hospice care, a moratorium would not interrupt that care.

NPHI's letter recommends that any moratorium be explicitly time-limited and paired with a clear path forward, allowing CMS to focus on identifying and removing fraudulent providers currently operating within the system while preventing new bad actors from entering. NPHI emphasizes that the fraud issue stems from a subset of providers exploiting gaps in oversight, not from the hospice model itself.

## What You Should Do

If you are a hospice provider, now is the time to ensure your enrollment documentation, billing practices, and compliance programs are current and well-documented. CMS is conducting unannounced site visits and expanding audits nationwide. Providers operating in good faith have the most to gain from a moratorium — it would remove fraudulent competitors — but the current enforcement environment means scrutiny is broad.

If you are a patient or family member, the key takeaway is that your current care is not at risk. A moratorium on new enrollments would not affect providers already in the Medicare program. If you have concerns about whether a hospice provider is legitimate, you can verify enrollment status through the Medicare.gov Care Compare tool.

Stay current through authoritative sources like CMS.gov and HHS.gov, where official announcements will be published if a moratorium is enacted.

## The Bottom Line

What began as a policy rumor has become a formal, industry-backed request to federal regulators — and the scale of the fraud driving it is well-documented and growing. As of April 2026, no hospice enrollment moratorium has been announced, but the conditions that would prompt one are clearly in place. Whether you're a provider or a patient, understanding what this policy tool does — and doesn't do — is the best preparation you can have.

---

type: article

title: Where To File for Unemployment Benefits in Every State

url: https://benefitkarma.com/articles/benefits-by-state/state-unemployment-offices

updated: 2026-05-13

---

# Where To File for Unemployment Benefits in Every State

If you need unemployment benefits, the first step is contacting your state workforce agency. Each state runs its own program, which means applications, payment amounts, and timelines vary depending on where you live.

The good news? You don’t have to hunt for the right website or phone number. We’ve pulled together a complete, up-to-date directory of every state unemployment office, plus Washington, D.C. and U.S. territories.

If you want more step-by-step guidance on applying, qualifying, and maximizing your benefits, BenefitKarma helps you stay informed with the latest updates and best practices across programs nationwide.

## All state unemployment offices (A–Z)

### Alabama – Alabama Unemployment Compensation Claimant Portal

- File/manage claim: https://adol.alabama.gov/claimants/

- Phone: (866) 234-5382

### Alaska – Alaska UI Claimant Services

- File/manage claim: https://bif.dol.alaska.gov/bif/

- Phone: (888) 252-2557

### Arizona – Arizona UI Benefits Portal (PUA/UI)

- File/manage claim: https://des.az.gov/services/employment/unemployment-individual

- Phone: (877) 600-2722

### Arkansas – Arkansas EZARC Unemployment Portal

- File/manage claim: https://dws.arkansas.gov/unemployment/

- Phone: (844) 908-2178

### California – California UI Online (EDD)

- File/manage claim: https://edd.ca.gov/en/unemployment/

- Phone: (800) 300-5616

### Colorado – Colorado MyUI+

- File/manage claim: https://cdle.colorado.gov/myui-plus

- Phone: (303) 318-9000

### Connecticut – Connecticut ReEmployCT

- File/manage claim: https://portal.ct.gov/dol/unemployment-benefits

- Phone: (860) 263-6000

### Delaware – Delaware UI Claimant Portal

- File/manage claim: https://uics.delawareworks.com

- Phone: (302) 761-8446

### Florida – Florida CONNECT Reemployment System

- File/manage claim: https://reconnect.commerce.fl.gov/

- Phone: (833) 352-7759

### Georgia – Georgia MyUI Claimant Portal

- File/manage claim: https://dol.georgia.gov/file-unemployment-insurance-claim

- Phone: (877) 709-8185

### Hawaii – Hawaii UI Claimant Services

- File/manage claim: https://huiclaims.hawaii.gov

- Phone: (808) 586-8970

### Idaho – Idaho Claimant Portal

- File/manage claim: https://labor.idaho.gov/claimantportal

- Phone: (208) 332-8942

### Illinois – Illinois IDES Claimant Portal

- File/manage claim: https://ides.illinois.gov/unemployment

- Phone: (800) 244-5631

### Indiana – Indiana Uplink Claimant Self-Service

- File/manage claim: https://uplink.in.gov/CSS

- Phone: (800) 891-6499

### Iowa – Iowa UI Claimant Portal

- File/manage claim: https://workforce.iowa.gov/unemployment

- Phone: (866) 239-0843

### Kansas – Kansas UI Claimant Portal

- File/manage claim: https://uiassistance.getkansasbenefits.gov

- Phone: (800) 292-6333

### Kentucky – Kentucky UI Portal

- File/manage claim: https://uiclaimsportal.ky.gov/

- Phone: (502) 564-2900

### Louisiana – Louisiana HiRE Portal

- File/manage claim: https://www.louisianaworks.net/hire/

- Phone: (866) 783-5567

### Maine – Maine ReEmployME

- File/manage claim: https://reemployme.maine.gov

- Phone: (800) 593-7660

### Maryland – Maryland BEACON UI Portal

- File/manage claim: https://beacon.labor.maryland.gov

- Phone: (667) 207-6520

### Massachusetts – Massachusetts UI Online

- File/manage claim: https://uionline.detma.org

- Phone: (877) 626-6800

### Michigan – Michigan MiWAM Portal

- File/manage claim: https://miwam.unemployment.state.mi.us

- Phone: (866) 500-0017

### Minnesota – Minnesota UI Claimant Portal

- File/manage claim: https://www.uimn.org

- Phone: (651) 296-3644

### Mississippi – Mississippi MDES Portal

- File/manage claim: https://reemployms.mdes.ms.gov/cp/landing

- Phone: (888) 844-3577

### Missouri – Missouri UInteract

- File/manage claim: https://uinteract.labor.mo.gov

- Phone: (800) 320-2519

### Montana – Montana UI eServices

- File/manage claim: https://uieservices.mt.gov

- Phone: (406) 444-2545

### Nebraska – Nebraska UI Claimant Portal

- File/manage claim: https://dol.nebraska.gov/UIBenefits

- Phone: (402) 458-2500

### Nevada – Nevada UI Claimant Portal

- File/manage claim: https://ui.nv.gov

- Phone: (888) 890-8211

### New Hampshire – New Hampshire UI Claimant Portal

- File/manage claim: https://www.nhes.nh.gov/individuals/file-unemployment-benefits

- Phone: (603) 271-7700

### New Jersey – New Jersey UI Claimant Portal

- File/manage claim: https://myunemployment.nj.gov

- Phone: (856) 507-2340

### New Mexico – New Mexico UI Claimant Portal

- File/manage claim: https://www.jobs.state.nm.us

- Phone: (877) 664-6984

### New York – New York UI Online Services

- File/manage claim: https://unemployment.labor.ny.gov

- Phone: (888) 209-8124

### North Carolina – North Carolina DES Portal

- File/manage claim: https://www.des.nc.gov/individuals/apply-ui

- Phone: (888) 737-0259

### North Dakota – North Dakota UI Portal

- File/manage claim: https://www.jobsnd.com/unemployment-individuals

- Phone: (701) 328-4995

### Ohio – Ohio UI Claimant Portal

- File/manage claim: https://unemployment.cmt.ohio.gov

- Phone: (877) 644-6562

### Oklahoma – Oklahoma UI Claimant Portal

- File/manage claim: https://unemployment.state.ok.us

- Phone: (800) 555-1554

### Oregon – Oregon Frances Online System

- File/manage claim: https://frances.oregon.gov

- Phone: (877) 345-3484

### Pennsylvania – Pennsylvania UC Portal

- File/manage claim: https://benefits.uc.pa.gov

- Phone: (888) 313-7284

### Rhode Island – Rhode Island UI Online

- File/manage claim: https://beta.uionline.dlt.ri.gov/

- Phone: (401) 415-6772

### South Carolina – South Carolina DEW Portal

- File/manage claim: https://scuihub.dew.sc.gov/CSS/CSSLogon.htm

- Phone: (866) 831-1724

### South Dakota – South Dakota UI Claimant Portal

- File/manage claim: https://dlr.sd.gov/ui

- Phone: (605) 626-2452

### Tennessee – Tennessee Jobs4TN Portal

- File/manage claim: https://jobs4tnui.tn.gov/claimant/_/

- Phone: (844) 224-5818

### Texas – Texas UI Claimant Portal

- File/manage claim: https://www.twc.texas.gov/services/apply-benefits

- Phone: (800) 939-6631

### Utah – Utah UI Claimant Portal

- File/manage claim: https://jobs.utah.gov/ui

- Phone: (801) 526-4400

### Vermont – Vermont UI Claimant Portal

- File/manage claim: https://labor.vermont.gov/unemployment-insurance

- Phone: (877) 214-3330

### Virginia – Virginia UI Claimant Portal

- File/manage claim: https://uidirect.vec.virginia.gov

- Phone: (866) 832-2363

### Washington – Washington eServices Portal

- File/manage claim: https://secure.esd.wa.gov

- Phone: (800) 562-2308

### West Virginia – WorkForce WV Portal

- File/manage claim: https://uc.workforcewv.org

- Phone: (800) 252-5627

### Wisconsin – Wisconsin UI Claimant Portal

- File/manage claim: https://my.unemployment.wisconsin.gov

- Phone: (844) 910-3661

### Wyoming – Wyoming UI Claimant Portal

- File/manage claim: https://wyui.wyo.gov

- Phone: (307) 473-3789

---

## District of Columbia & Territories

Try it: Find Benefits — See benefits available in your state.

### Washington, D.C. – DC UI Claimant Portal

- File/manage claim: https://does.dcnetworks.org

- Phone: (202) 724-7000

### Puerto Rico – Puerto Rico UI Portal

- File/manage claim: https://desempleo.trabajo.pr.gov/reclamantes/(S(obcub2emei4muuhupywg5kzo))/Inicio.aspx

- Phone: (787) 754-5353

### U.S. Virgin Islands – USVI UI Portal

- File/manage claim: https://unemployment.vidol.gov/

- Phone: (340) 773-1994

### Guam – Guam UI Claimant Portal

- File/manage claim: https://dol.guam.gov/unemployment/

- Phone: (671) 475-7000

---

## How to use this list

- Always apply through your state’s portal (above)

- Create an account before filing

- File weekly certifications to keep payments active

- Call only if you’re locked out, denied, or flagged

---

## Why this matters

Every state system is different, and using the wrong page can delay your benefits by weeks.

This list cuts straight to the exact pages that matter, so you can:

- apply faster

- avoid scams or outdated links

- get paid sooner

---

type: article

title: Unemployment Identity Theft: What to Look For

url: https://benefitkarma.com/articles/income-employment/unemployment-fraud-identity-theft

updated: 2026-07-01

---

# Unemployment Identity Theft: What to Look For

Unemployment benefits are meant to help when you’re between jobs, but scammers have found ways to exploit the system. One of the most common schemes right now? Filing fraudulent unemployment claims using stolen personal information, like your Social Security number.

If you receive a letter about unemployment benefits you never applied for, don’t brush it off. It may seem like a mistake, but it’s often a sign of identity theft, and ignoring it can lead to bigger problems like tax issues, delayed refunds, or even wage garnishment. The good news is that there are clear steps you can take right away to protect yourself.

If you want to stay informed on scams, benefits, and how to protect your finances, BenefitKarma breaks down what matters without the confusing jargon. Here’s what to do if this happens to you.

## Why this happens (and why it matters)

Unemployment fraud surged during and after the pandemic, and it’s still happening today. Scammers use stolen personal information, often from data breaches, to file claims in someone else’s name and collect benefits.

You might only find out when:

- Your employer gets notified of a claim you didn’t file

- Your state unemployment agency sends you a letter

- You receive unexpected tax forms (like a 1099-G for unemployment income)

The risk goes beyond stolen benefits. Fraud like this can:

- Delay your tax refund

- Trigger IRS issues if income is reported under your name

- Damage your credit if your identity is used elsewhere

That’s why acting quickly is critical.

## Step 1: Report it to your employer

Try it: Find Benefits — Explore income, employment and tax benefits available to you.

Start with your employer as soon as you notice the issue. They may have already received notice of the fraudulent claim and can confirm it wasn’t legitimate.

Employers often work directly with state agencies to flag fraud, so this step helps stop the claim faster.

## Step 2: Contact your state unemployment agency

Next, report the fraud to your state workforce or unemployment office. Most states have dedicated fraud reporting tools online.

This step is key because it:

- Stops payments from continuing

- Flags your identity in the system

- Helps prevent future fraudulent claims in your name

Be prepared to verify your identity and confirm you didn’t apply.

## Step 3: Report identity theft to the FTC

Go to IdentityTheft.gov and file a report. This is the federal government’s official identity theft recovery site.

You’ll get a personalized recovery plan with step-by-step instructions based on your situation. It’s free and widely recommended by experts.

## Step 4: Freeze your credit (free and powerful)

A credit freeze makes it much harder for scammers to open new accounts in your name.

Contact all three major credit bureaus:

- Equifax

- Experian

- TransUnion

Freezing your credit does not affect your score, and you can lift the freeze anytime.

## Step 5: Check your credit reports regularly

Visit AnnualCreditReport.com to access your free credit reports (currently available weekly).

Look for:

- Accounts you don’t recognize

- Hard inquiries you didn’t authorize

- Changes to your personal information

If you spot errors, dispute them with the credit bureau immediately.

## Step 6: Protect your taxes with an IRS PIN

If your Social Security number has been used fraudulently, consider setting up an IRS Identity Protection PIN.

This six-digit code helps prevent someone from filing a tax return in your name and stealing your refund. It’s especially useful after unemployment-related identity theft.

## Common mistakes to avoid

When this happens, timing matters. Avoid these common missteps:

- Ignoring the letter or assuming it’s a mistake

- Waiting too long to report the fraud

- Only reporting it to one agency instead of all three (employer, state, FTC)

- Skipping credit monitoring

Even a short delay can make recovery harder.

## Bottom line

If you get a notice about unemployment benefits you didn’t file, treat it as identity theft until proven otherwise.

Take these steps right away:

- Report it to your employer

- Contact your state unemployment agency

- File a report at IdentityTheft.gov

- Freeze your credit and monitor your reports

- Consider setting up an IRS PIN

Acting quickly can stop the fraud, protect your finances, and prevent long-term damage.

For more straightforward guides on benefits, scams, and how to protect your money, keep checking back with BenefitKarma; we’ll keep you in the know.

---

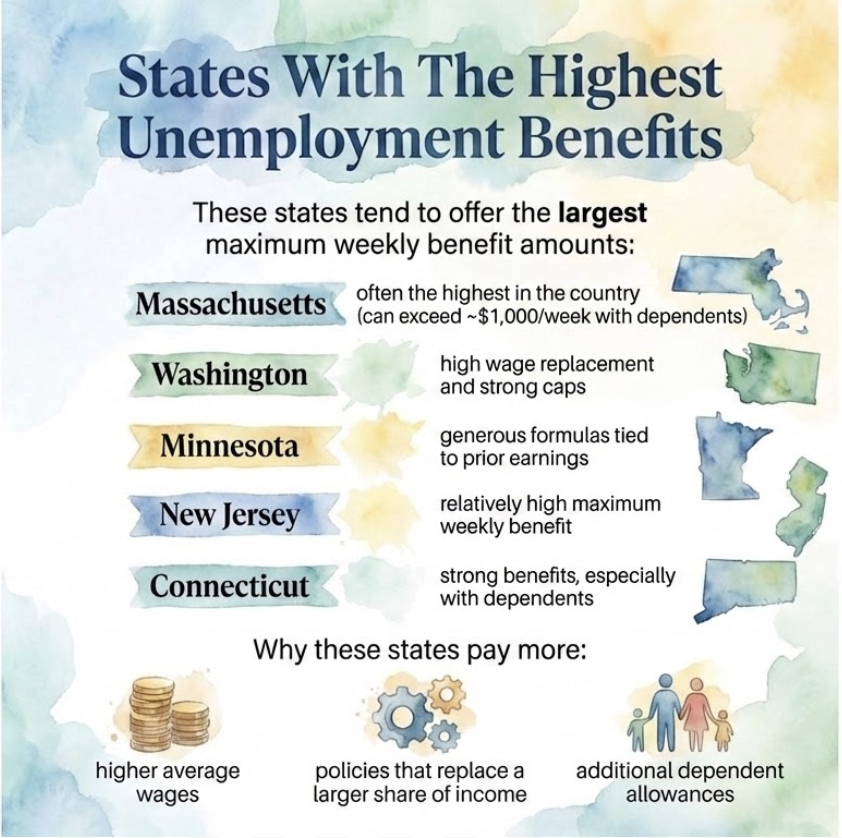

type: article

title: State Unemployment Benefits In 2026: Why Payouts And Rules Vary More Than You Think

url: https://benefitkarma.com/articles/income-employment/state-unemployment-benefits-in-2026

updated: 2026-07-01

---

# State Unemployment Benefits In 2026: Why Payouts And Rules Vary More Than You Think

State unemployment benefits are a critical safety net for workers who lose their jobs, but in 2026, where you live matters more than ever.

A recent CNBC report highlights how dramatically unemployment benefits can differ across states, from how much you receive to how long payments last. If you’re navigating job loss or planning ahead, understanding these differences can make a real financial impact.

Unemployment insurance (UI) is a joint federal-state program, but states control most of the rules. That means eligibility requirements, weekly payments, and benefit durations can vary widely. With inflation, labor market shifts, and state-level policy changes all in play, 2026 has become a year where those differences are especially noticeable.

Want to stay on top of changes like this? BenefitKarma keeps you informed on how government benefits work and how to make the most of them.

## Why Unemployment Benefits Vary By State

The biggest takeaway from the CNBC report: there is no single “standard” unemployment benefit in the U.S.

Each state sets its own formula based on factors like:

- prior earnings

- state wage levels

- local unemployment rates

- policy decisions made by state legislatures

For example, some states replace a higher percentage of your previous wages, while others cap benefits at relatively low amounts. According to CNBC, the maximum weekly benefit can range from a few hundred dollars to over $1,000 depending on the state.

That means two workers with similar salaries could receive very different support simply based on where they live.

## How Much You Can Receive

Try it: Find Benefits — Explore income, employment and tax benefits available to you.

Weekly benefit amounts are typically calculated as a percentage of your recent earnings, often around 30% to 50% of your average weekly wage—but caps vary significantly.

Examples from the report show:

- lower-benefit states may cap weekly payments under $400

- higher-benefit states can exceed $800–$1,000 per week

Some states also provide additional allowances for dependents, while others do not.

The key point is that your benefit is not just about what you earned; it’s also about your state’s policy choices.

## How Long Benefits Last

Benefit duration is another major difference.

Most states offer up to 26 weeks of unemployment benefits, but that’s not universal anymore. Some states have reduced durations, offering:

- as few as 12 to 20 weeks in certain cases

- variable durations tied to unemployment rates

During periods of high unemployment, extended benefits may kick in, but these are not guaranteed and often require federal or state action.

According to CNBC, several states have moved toward shorter benefit periods in recent years, which can leave workers with less time to find new employment.

## Eligibility Requirements To Know

Even qualifying for unemployment benefits can depend heavily on where you live.

Common requirements include:

- earning a minimum amount during a “base period”

- losing your job through no fault of your own

- being actively available and searching for work

However, states differ in how strictly they enforce these rules. Some have:

- stricter job search reporting requirements

- tighter definitions of “suitable work”

- additional verification steps

These differences can affect whether you qualify and how long you continue receiving benefits.

## What Unemployment Benefits Pay For

Unemployment benefits are designed to cover basic living expenses while you search for work.

They can help pay for:

- rent or mortgage payments

- groceries and essential household items

- utilities like electricity and water

- transportation costs related to job searching

However, because benefits often replace only a portion of your income, many households still need to adjust spending or seek additional support programs.

## How To Apply For Unemployment Benefits

Applying is done through your state’s unemployment office, usually online.

Here’s a general step-by-step (but we've got a full "how to sign up for unemployment" article ready with more detail):

- file a claim with your state’s UI agency

- provide employment history and income details

- verify your identity and job separation reason

- certify weekly (or biweekly) that you’re still eligible

- report job search activities if required

Processing times vary, but many states take 2–4 weeks to issue the first payment (longer if there are verification issues).

## How Unemployment Benefits Compare To Other Programs

Unemployment insurance is different from other support programs like:

- Supplemental Nutrition Assistance Program (SNAP), which helps with food costs

- Temporary Assistance for Needy Families (TANF), which provides limited cash aid for low-income families

Unlike these programs, unemployment benefits are:

- based on your work history

- temporary by design

- tied to active job searching

Many people use unemployment benefits alongside these programs to cover gaps.

## What To Do If Your Benefits Run Out Or Are Denied

If your benefits are denied:

- you can usually file an appeal through your state agency

- you may need to provide additional documentation or attend a hearing

If your benefits run out:

- check for extended benefits in your state

- explore other assistance programs like SNAP or housing support

- consider workforce training programs that may offer stipends

Understanding your options early can help prevent financial stress later.

## The Bottom Line

Unemployment benefits can be a lifeline, but they’re not one-size-fits-all. The CNBC report makes it clear: your state plays a major role in how much help you receive and how long it lasts.

If you’re working, it’s worth understanding your state’s rules before you ever need them. And if you’re currently unemployed, knowing the specifics can help you plan your next steps with more confidence.

For more clear, practical breakdowns of benefits like unemployment insurance, stay connected with BenefitKarma.

---

type: article

title: LIHEAP on the Chopping Block in Proposed 2027 Budget

url: https://benefitkarma.com/articles/benefits-in-the-news/liheap-cuts-set-for-2027-budget

updated: 2026-07-01

---

# LIHEAP on the Chopping Block in Proposed 2027 Budget

Millions of Americans rely on help to keep the lights on, the heat running, and their homes safe during extreme weather. But a new federal budget proposal could change that.

The fiscal year 2027 budget put forward by President Donald Trump calls for eliminating funding for the Low-Income Home Energy Assistance Program (LIHEAP) — a long-standing program that helps low-income households pay their energy bills.

If approved by Congress, this change could leave many families scrambling to cover essential utility costs.

So what exactly is LIHEAP, who depends on it, and what can you do if these changes move forward? Here’s what to know.

BenefitKarma keeps you up-to-date on major benefit changes like this so you can plan ahead and protect your household.

## What is LIHEAP and why it matters

The Low-Income Home Energy Assistance Program (LIHEAP) is a federally funded program that helps eligible households manage home energy costs.

It supports both heating and cooling needs, which is especially important in areas with extreme winters or summers.

We go into detail about how this program works, and what it helps pay for in our LIHEAP article.

### What LIHEAP helps pay for

- Monthly heating and cooling bills

- Emergency energy assistance (like preventing shutoffs)

- Crisis situations (such as no heat in winter)

- Minor home energy upgrades (like weatherization improvements)

For many households, LIHEAP isn’t just helpful—it’s essential for health and safety.

## Why the program is at risk

Try it: Find Benefits — Explore the full benefits library.

The proposed budget eliminates LIHEAP as part of broader efforts to reprioritize federal spending.

The program is currently administered by the U.S. Department of Health and Human Services (HHS), which distributes funds to states. Those states then run their own LIHEAP programs based on federal guidelines.

If funding is removed:

- States would lose federal support for energy assistance

- Many existing programs would shrink—or disappear entirely

- Households would need to find alternative help quickly

This would mark a major shift away from decades of federal support for basic utility needs.

## How many people could be affected

The numbers help show just how large this impact could be.

- 6.1 million households received LIHEAP benefits in 2026

- The average benefit was about $401 per household

- Only about 20% of eligible households currently receive help

That last point is critical.

Even with funding, most eligible households already don’t receive assistance due to limited resources. If LIHEAP is eliminated:

- That 20% drops to 0%

- Millions of households lose direct support

- Many more who might qualify in the future lose access entirely

## What losing LIHEAP could mean for households

### 1. Higher energy costs out of pocket

Without LIHEAP, households would need to cover full utility bills—often during the most expensive seasons.

### 2. Increased risk of shutoffs

Emergency assistance helps prevent electricity or heating disconnections. Without it, more families could face utility shutoffs, especially in winter or heat waves.

### 3. Health and safety risks

Energy isn’t just a convenience—it’s tied to:

- Safe indoor temperatures

- Medical equipment (like oxygen machines)

- Food storage (refrigeration)

Losing assistance could increase health risks for seniors, children, and people with disabilities.

Households may be forced to choose between paying utility bills, buying groceries, or covering rent or medication.

## What you should do right now

If you currently receive LIHEAP (or think you might qualify), here are steps you can take to prepare:

### 1. Stay informed on the budget process

This proposal is not final yet. Congress must review and approve the budget before changes take effect.

### 2. Look into local assistance programs

Even if federal funding changes, some support may still exist through:

- State or county programs

- Utility company assistance plans

- Local nonprofits and charities

Search for:

- “energy assistance near me”

- “utility bill help [your state]”

### 3. Contact your representatives

You can share your perspective with elected officials. Budget decisions can change, and public input can matter.

### 4. Reduce energy costs where possible

Consider:

- Weatherproofing your home

- Using energy-efficient appliances

- Asking your utility provider about budget billing plans

### 5. Apply while funding is still available

If LIHEAP is still active in your area, applying now could help you secure assistance before any changes happen.

## How this compares to other benefit programs

Unlike programs such as food assistance or healthcare, LIHEAP is:

- Discretionary funding (not guaranteed year to year)

- Distributed through state-run systems

- Often limited by available federal budgets

That’s why only a portion of eligible households receive help — and why proposals like this can have such a large impact.

## The bottom line

The proposed elimination of LIHEAP would remove a critical source of support for millions of low-income households struggling with energy costs.

While the budget is still under review, the potential impact is significant—especially for those already facing tight financial situations.

If this change moves forward, households will need to rely more heavily on local programs, nonprofits, and personal budgeting strategies to cover essential energy needs.

Staying informed is your best defense. BenefitKarma will continue tracking this proposal and other major benefit changes so you always know what’s coming and how to respond.

---

type: article

title: Why Social Security Fairness Act Payments are Taking Longer than Expected

url: https://benefitkarma.com/articles/income-employment/extension-for-fairness-act-payouts

updated: 2026-07-01

---

# Why Social Security Fairness Act Payments are Taking Longer than Expected

Televised Senate hearings don’t usually make headlines, but when they involve Social Security benefits, people pay attention.

That’s exactly what happened when several senators called for more time to complete retroactive payments under the Social Security Fairness Act. For many retirees, this raised an immediate concern: Are benefits being delayed again?

The short answer is yes, there are delays. But there’s also context, and importantly, there’s still progress being made.

If you’re affected, understanding what’s happening (and what to expect next) can help you stay prepared and not panicked.

BenefitKarma tracks changes like this so you can stay informed about the benefits that matter most to you.

## What the Social Security Fairness Act actually does

The Social Security Fairness Act was designed to fix a long-standing issue affecting public servants.

It repeals two major provisions:

### Government Pension Offset (GPO)

The Government Pension Offset reduced Social Security spousal or survivor benefits for people who also received a government pension.

### Windfall Elimination Provision (WEP)

The Windfall Elimination Provision reduced Social Security retirement benefits for workers who earned pensions from jobs not covered by Social Security.

### Who this affects

- Teachers

- Firefighters

- Police officers

- Other public sector workers

For years, these rules reduced benefits, even for people who paid into Social Security through other jobs.

The Fairness Act removes those reductions, allowing retirees to receive full benefits moving forward, plus retroactive payments for past underpayments.

## Why retroactive payments are delayed

Try it: Find Benefits — Explore income, employment and tax benefits available to you.

Fixing the problem is one thing; recalculating millions of benefits is another.

The Social Security Administration (SSA) has to:

- Recalculate benefits without WEP and GPO reductions

- Review individual work histories

- Adjust past payment records

- Issue retroactive payments

### The biggest issue: manual processing

Many of these cases require manual review, not automated updates.

That means:

- Each file may need individual attention

- Older records must be verified

- Complex benefit histories must be recalculated

This has created a backlog that’s larger (and slower-moving) than expected.

## Where things stand right now (April 2026)

The implementation of the Social Security Fairness Act is nearly complete, but a small percentage of cases remain in limbo.

Most payments are done: The SSA successfully automated the vast majority of recalculations in early 2025. By July 2025, over 3.1 million beneficiaries had already received their adjusted payments.

The Retroactive Window: The law was retroactive to January 2024. This means most eligible retirees received a large lump-sum payment in the spring of 2025 to cover the "back-pay" for all of 2024 and early 2025.

Current Delays: While the "March 2024" hurdles are long gone, the SSA is currently working through the final 5% of complex cases. These involve:

- Retirees with foreign pensions.

- Records requiring manual verification of earnings from the 1970s or 80s.

- New applicants who are currently fighting for the full 12 months of retroactivity (some are only being offered 6 months due to technicalities in the Social Security Act).

## What this means for your benefits in 2026

If you are eligible under the Fairness Act but haven't seen a change yet, here is the current reality:

- You are still entitled to the money: The law is permanent. If WEP or GPO reduced your check in the past, those reductions stopped being legal as of January 2024.

- Retroactive payments are still being issued: For the "complex" backlog, the SSA is still issuing lump sums throughout 2026.

- The "Six-Month" Dispute: There is currently a push by lawmakers (as of February 2026) to ensure that new applicants get the full year of retroactive pay back to Jan 2024, as the SSA has been limiting some new claims to only 6 months of back-pay.

## What you should do right now

Because we are now more than a year past the bill becoming law, "waiting and seeing" is no longer the best strategy.

- Review your 2025 Tax Forms: Your 1099 form received in January 2026 should reflect any retroactive lump sums paid out last year. If it doesn't, and your monthly check hasn't increased, your file may be stuck in manual review.

- File for Reconsideration: If you applied recently and were denied the full retroactive pay back to January 2024, advocates recommend filing Form SSA-561 (Request for Reconsideration) to protect your rights while Congress clarifies the timing rules.

- Verify your "Non-Covered" Pension: Ensure the SSA has the correct details of your government pension on file, as errors here are the leading cause of manual processing delays in 2026.

## How this compares to previous Social Security changes

Most Social Security updates are applied automatically. This situation is different.

Why?

- WEP and GPO changes affect millions of individual records

- Many cases involve decades-old earnings histories

- Systems were not built for this kind of large-scale recalculation

That’s why this rollout is slower than typical benefit adjustments.

## The bottom line

The delays tied to the Social Security Fairness Act are frustrating, but they don’t change the outcome.

Public servants affected by WEP and GPO are still set to receive the benefits they were previously denied. The process is just taking longer than expected due to the scale and complexity of recalculating payments.

Lawmakers are now stepping in to extend the timeline, which could help ensure that payments are processed correctly, even if it takes more time.

If you’re waiting, the most important thing to know is this: the benefits are still coming.

BenefitKarma will continue tracking updates to the Fairness Act and other major programs so you always know what’s happening and what to do next.

---

type: article

title: Stalled Heating Help: Senators Fight to Unlock $400M in Energy Funds

url: https://benefitkarma.com/articles/benefits-by-state/stalled-heating-help-40-senators-fight-to-unlock-400m-in-federal-energy-funds

updated: 2026-07-01

---

# Stalled Heating Help: Senators Fight to Unlock $400M in Energy Funds

Millions of families who rely on federal energy assistance are waiting on roughly $400 million in heating and cooling funds that the Trump administration has yet to release — and a bipartisan group of senators is demanding action now.

If you rely on government benefits to cover your household costs, BenefitKarma is a trusted source for clear, up-to-date information on programs like this one.

## What is LIHEAP and why does it matter?

The Low Income Home Energy Assistance Program, or LIHEAP, is a federal program that helps low-income households pay their heating and cooling bills. Congress created LIHEAP in 1981, and it has grown into one of the most widely supported programs in the federal safety net, delivering assistance to nearly six million households nationwide each year.

The program specifically targets households with members who are especially vulnerable to extreme temperatures — including people with disabilities, families with young children, and elderly residents, who are physiologically less able to regulate their body temperature.

In the midst of economic hardships, many recipients are also on the edge of a utility shutoff or already disconnected when they apply, making timely funding a matter of health and safety.

According to the National Energy Assistance Directors Association, the total amount owed across those households is approximately $21 billion — the highest level since 2021 and up roughly 30 percent since the end of 2023.

## What is happening with the $400 million?

Try it: Find Benefits — See benefits available in your state.

For fiscal year 2026, Congress appropriated $4.045 billion for LIHEAP — a $20 million increase over the previous year. On November 28, 2025, HHS released approximately $3.7 billion of that amount to states. The remaining roughly $400 million has not yet been distributed.

On March 12, 2026, a bipartisan group of 40 U.S. senators sent a letter to HHS Secretary Robert F. Kennedy Jr. urging the immediate release of the remaining funds. The letter was led by Senators Jack Reed (D-RI), Susan Collins (R-ME), and Lisa Murkowski (R-AK), a notably bipartisan trio that reflects how broadly supported LIHEAP has historically been in Congress.

In their letter, the senators warned that any delay would set back states' efforts to cover outstanding bills from energy emergencies, weatherize low-income homes, and plan for summer cooling programs. Home heating costs are expected to run 11 percent higher this coming winter compared to last year, intensifying the urgency.

The timing matters because this is not the first standoff over LIHEAP funds under the current administration.

- In April 2025, the Trump administration fired the entire LIHEAP program staff at HHS.

- On April 30, 2025, following sustained congressional pressure, HHS released $401.5 million in remaining FY2025 LIHEAP funds.

- As of May 1, 2025, states were able to draw down on their grants.

- The pattern — congressional pressure followed by eventual release — is now repeating with FY2026 funds.

## The bigger threat to LIHEAP

Beyond the immediate funding delay, there is a larger fight underway. The Trump administration has proposed eliminating LIHEAP entirely in its fiscal year 2026 budget, and federal LIHEAP staff who were fired in April 2025 have not been rehired, leaving states to run their programs with no federal training or guidance.

The White House has described LIHEAP as "unnecessary," arguing that the administration's energy policies will lower prices enough to make the program redundant. Budget experts and program administrators have pushed back sharply, noting that Congress controls appropriations and has funded LIHEAP at no less than $3 billion annually since 2009.

For now, Congress has continued to appropriate money for the program. Whether HHS releases those funds promptly — and how the program is administered without dedicated federal staff — remains an open question.

## What should you do?

If you receive LIHEAP assistance or think you might qualify, here are practical steps you can take right now.

Contact your state or local LIHEAP agency directly. States received the bulk of FY2026 funds in late November 2025 and may already be distributing benefits in your area. To find your state's program, visit the U.S. Department of Energy LIHEAP State Map of Contacts at energy.gov.

Check whether you are eligible. LIHEAP applications are currently open for all income-eligible households, with eligibility based on income, family size, and the availability of resources. Seniors and those receiving Social Security Disability or SSI benefits are encouraged to apply as early as possible, but applications are open to everyone through spring 2026 or until funding is exhausted.

Also contact your utility provider. Many electric and gas companies offer their own low-income assistance programs, budget billing options, or hardship funds that can help bridge the gap while you wait on federal or state aid.

Keep your paperwork organized. When funds are released and your state agency begins processing applications, having your utility bills, income documentation, and household information ready will help you get assistance faster.

## The bottom line

Nearly six million households depend on LIHEAP to avoid making impossible choices between paying energy bills and covering food, medical care, or other essentials. The $400 million still sitting with HHS is congressionally approved money that states say they are ready to deploy immediately.

With 40 senators pushing for release and a pattern from 2025 showing that congressional pressure has moved the administration before, there is reason to expect the funds will eventually reach families.

But with no dedicated federal staff and an administration that has proposed ending the program altogether, the situation bears close watching. BenefitKarma will continue tracking this as it develops.

---

type: article

title: Is Section 8 Mandatory? New Court Ruling Explained

url: https://benefitkarma.com/articles/benefits-in-the-news/is-section-8-mandatory-court-ruling

updated: 2026-07-01

---

# Is Section 8 Mandatory? New Court Ruling Explained

A landmark court ruling is shaking up the rules around Section 8 housing — and if you're a landlord or a tenant who relies on housing vouchers, you need to know what changed.

On March 5, 2026, New York's Appellate Division issued a unanimous decision declaring that the New York State Human Rights Law violates the Fourth Amendment to the extent it forces landlords to participate in the federal Housing Choice Voucher (HCV) program, commonly known as Section 8.

It is the first time any appellate court in the country has struck down a "source of income" anti-discrimination law on constitutional grounds. Legal experts expect the ruling to ripple far beyond New York, potentially affecting similar laws in at least 19 states and more than 130 municipalities nationwide.

If you want to stay on top of changes like this across major benefits programs, BenefitKarma is a trusted source for clear, up-to-date information.

## What is Section 8 and why does this matter?

Section 8, formally known as the Housing Choice Voucher program, was created under the Housing Act of 1937. The program helps low-income families afford safe housing in the private rental market by subsidizing a portion of their rent.

Today, roughly 5 million people in 2.2 million low-income households receive HCV assistance, backed by approximately $18.9 billion in annual federal funding.

In recent years, many states and cities — including New York — passed "source of income" (SOI) laws making it illegal for landlords to refuse tenants simply because they pay with a housing voucher. The intent was to prevent voucher holders from being shut out of neighborhoods and to expand access to affordable housing.

The March 5 ruling says that approach goes too far. The Appellate Division held that compelling a private landlord to participate in a federal inspection program — as Section 8 requires — forces them to waive Fourth Amendment protections against warrantless searches.

The court found that because Section 8 regulations do not include a mechanism for inspectors to obtain a warrant if a landlord refuses entry, mandating participation in the program is unconstitutional.

## What led to this ruling?

Try it: Find Benefits — Explore the full benefits library.

The legal groundwork was laid over several years. In June 2023, a trial court in Tompkins County, New York, dismissed an Attorney General enforcement action against a landlord who declined to participate in Section 8. That court ruled in favor of the landlord on Fourth Amendment grounds in People v. Commons West, LLC. A second decision in December 2024 reaffirmed that the Human Rights Law was "facially unconstitutional" on the same basis. The Appellate Division's March 5, 2026 ruling made those conclusions binding statewide.

A separate but related case in Missouri reinforced the trend. In February 2025, a federal court reached a similar conclusion regarding a Kansas City ordinance — though Missouri subsequently passed a state law that made the city ordinance moot before the case could proceed further.

## What does this mean for landlords?

In New York, landlords can no longer face legal penalties for declining to participate in Section 8 solely because of the program's inspection requirements. The New York State Division of Human Rights is currently reviewing how the ruling affects pending source-of-income cases.

If you are a landlord in New York or another state with similar SOI laws, it is critical to understand that this ruling applies specifically to New York State at this stage and may be further appealed to the New York State Court of Appeals. Laws in other states have not been formally struck down — yet. The ruling may prompt legal challenges in other jurisdictions, but each state's situation will depend on its own laws and court proceedings.

## What does this mean for tenants?

For the approximately 5 million Americans who rely on housing vouchers, this ruling raises real concerns. If landlords in New York — and potentially other states — are no longer legally required to accept vouchers, finding willing landlords could become harder.

It is worth noting that many landlords do choose to participate in Section 8 voluntarily, and nothing in this ruling prevents them from continuing to do so. Federal HCV funding has not changed as a result of this ruling. However, in a tight housing market, reduced landlord participation could mean fewer housing options for voucher holders.

If you receive Section 8 assistance, reaching out to your local Public Housing Authority (PHA) is the best first step. Your PHA can explain how this may affect your current voucher, what rights you retain, and what resources are available if you need help finding a participating landlord. Make sure your contact information on file with your PHA is current so you receive any updates directly.

## The bottom line

The March 5, 2026 Appellate Division ruling is the first of its kind at the appellate level in the United States, and it carries real consequences for how source-of-income protections are enforced going forward. For landlords in New York, it removes a legal obligation that many argued infringed on their property rights. For tenants with housing vouchers, it adds uncertainty to an already difficult housing landscape.

This case is likely to be appealed further, and similar legal challenges are expected in other states. BenefitKarma will continue tracking developments as they unfold.

---

type: article

title: How IRMAA Made Your Social Security Increase Look Smaller

url: https://benefitkarma.com/articles/income-employment/social-security-irmaa

updated: 2026-07-01

---

# How IRMAA Made Your Social Security Increase Look Smaller

If you received your first Social Security check of 2026 and thought the cost-of-living increase looked smaller than advertised, you are not imagining it.

For a significant number of retirees — especially those with higher incomes — Medicare surcharges called IRMAA are quietly eating into that increase before it ever reaches their bank account.

If you want to stay on top of changes like this across major benefits programs, BenefitKarma is a trusted resource for clear, up-to-date information.

## What is IRMAA?

IRMAA stands for Income-Related Monthly Adjustment Amount. It is an additional charge that higher-income Medicare beneficiaries pay on top of their standard Part B and Part D (prescription drug) premiums.

The Social Security Administration determines your IRMAA based on your Modified Adjusted Gross Income (MAGI) from two years prior, which means your 2024 tax return is what determines whether you owe a surcharge in 2026.

According to Medicare Resources, about 5.1 million Medicare beneficiaries — roughly 7% of all enrollees — paid Part B IRMAA surcharges in 2025. It is not a charge most people will face, but for those who do, it can significantly reduce the net value of any Social Security increase.

## Why is this a problem right now?

Try it: Find Benefits — Explore income, employment and tax benefits available to you.

Social Security's 2026 cost-of-living adjustment came in at 2.8%. On paper, that sounds like a meaningful raise. In practice, it is being undercut from two directions at once.

First, the standard Medicare Part B premium. The 2026 standard premium is $202.90 per month, up $17.90 from $185.00 in 2025 — the first time Part B has crossed $200. For the average retiree receiving $2,071 per month in Social Security, Medicare Part B now consumes 9.8% of their check before any supplemental coverage. Research from the Boston College Center for Retirement Research found that Medicare premiums eat more than 25% of the 2026 COLA increase.

Second, for those subject to IRMAA, the situation is more severe. A retiree in the second IRMAA bracket pays $284.10 per month for Part B alone — nearly $100 more than the standard premium.

A 2.8% COLA cannot meaningfully offset that burden, especially since IRMAA thresholds are based on income from two years prior, meaning a retiree who had a high-income year in 2024 is paying elevated premiums today even if their financial situation has since changed.

> READ: Social Security COLA 2027 Could Be Smaller Than Many Retirees Hoped

>

>

## Who gets hit with IRMAA in 2026?

For 2026, the IRMAA income brackets and surcharges increased by approximately 3% and 9%, respectively. The 2026 IRMAA thresholds are $109,000 for a single person and $218,000 for a married couple filing jointly.

IRMAA is calculated on a sliding scale with five income brackets, topping out at $500,000 for individual filers and $750,000 for married couples filing jointly. For those subject to IRMAA, total monthly Part B premiums range from $284.10 to $689.90. Part D surcharges range from $14.50 to $91.00 per month.

One thing that catches retirees off guard is the "cliff" nature of these brackets. If your income crosses into the next bracket by even one dollar, your Medicare premiums can jump by over $1,000 per year. If you are married and both spouses are on Medicare, that same $1 increase can trigger a jump of over $1,000 per year for each of you.

It is also worth knowing that IRMAA can be triggered by one-time income events — not just a permanently higher salary. A large Roth conversion, a business sale, or a required minimum distribution in a single year can push premiums higher for two years running.

## What can you do?

If you received an IRMAA notice and believe it is based on income that no longer reflects your situation, you have options.

You have 60 days from receiving an IRMAA notice to file an appeal with the Social Security Administration. Common reasons to appeal include incorrect or outdated tax information or a life-changing event such as loss of income, death of a spouse, marriage, or divorce.

To start the process, contact the SSA at 800-772-1213 (TTY: 800-325-0778), Monday through Friday, 8 a.m. to 7 p.m.

You can also complete the Medicare IRMAA Life-Changing Event form (SSA-44) directly through the SSA.

If you are still working or have flexibility in your income, there are planning strategies worth exploring with a financial advisor — things like timing Roth conversions, increasing contributions to tax-deferred accounts, or making qualified charitable distributions directly from an IRA if you are 70½ or older.

These approaches can help lower your MAGI and potentially keep you below an IRMAA threshold. BenefitKarma is not a financial advisor, and decisions like these deserve personalized guidance.

## The bottom line

IRMAA is not a penalty; it is a built-in feature of Medicare designed to have higher-income beneficiaries pay a larger share of program costs. But the combination of a modest 2.8% COLA, a Part B premium that crossed $200 for the first time in 2026, and IRMAA surcharges based on income from two years ago can leave retirees feeling like their raise disappeared before they saw it.

Understanding the rules — and knowing that appeals are available when your income has genuinely changed — puts you in a better position to manage what you actually take home.

---

type: article

title: Tax Refund Season 2026 Looks to Be a Big One: Here's Why

url: https://benefitkarma.com/articles/benefits-in-the-news/tax-refund-season-2026

updated: 2026-07-01

---

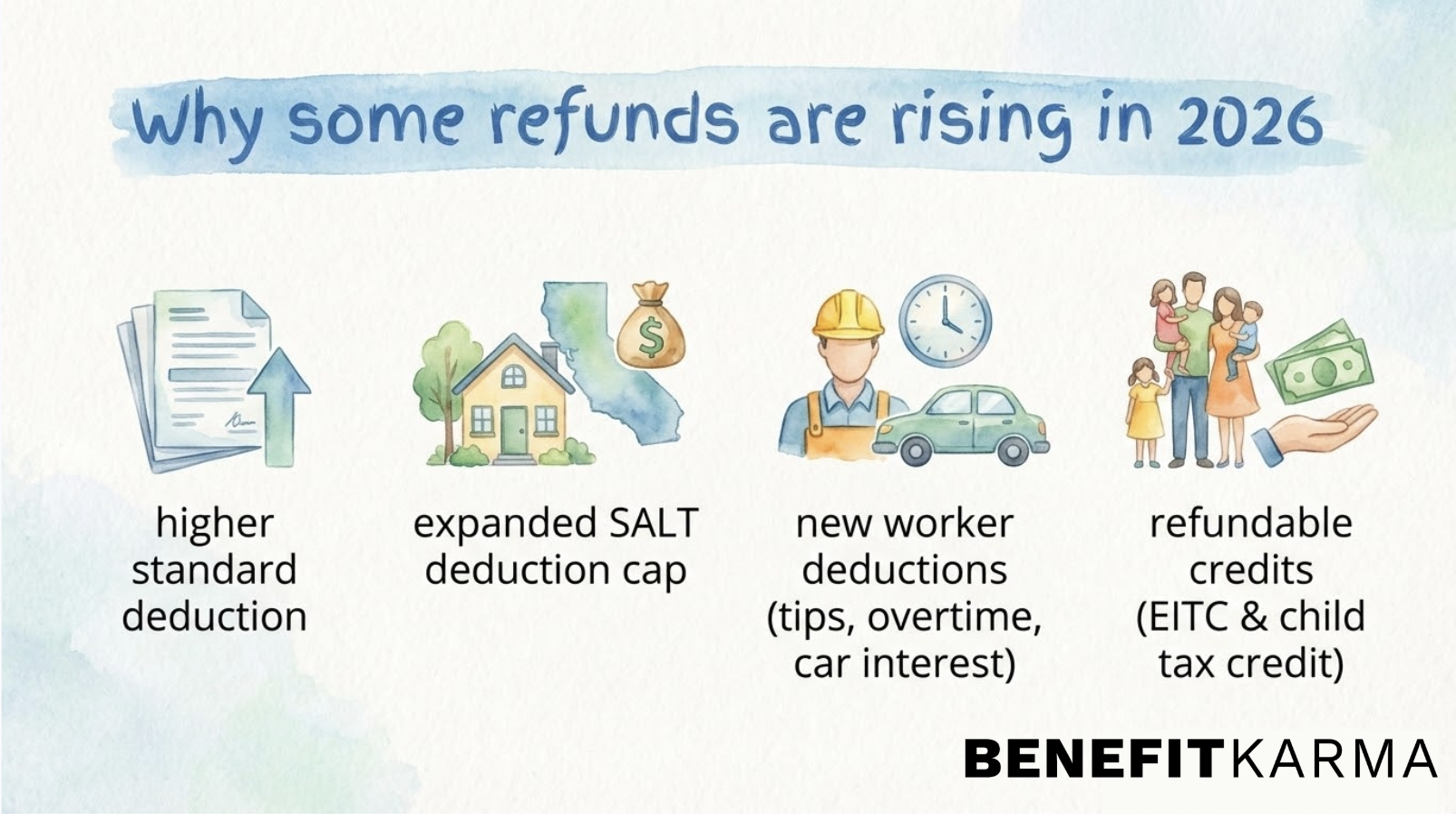

# Tax Refund Season 2026 Looks to Be a Big One: Here's Why

Tax refund season is officially underway, and early data suggests many filers could see larger checks this year.

According to the Internal Revenue Service (IRS), average refunds in early February were running about 11% higher than the same time last year — around $2,290 as of early filing data — though those numbers shift as more returns are processed.

What’s driving the increase? A combination of updated federal tax provisions, higher standard deductions, and refundable tax credits like the Earned Income Tax Credit (EITC) and the Additional Child Tax Credit. Together, these changes are reshaping what many households can expect back.

Tax law updates can feel overwhelming. That’s where we come in. At BenefitKarma, we track changes across government programs and break them down into simple, practical steps so you can file with confidence — and keep more of what you earn.

## Why are refunds higher this year?

Refunds increase when one of three things happens:

- You paid more in taxes than you owed

- You qualify for new or larger deductions

- You qualify for refundable tax credits

Several recent federal updates are influencing 2026 refunds:

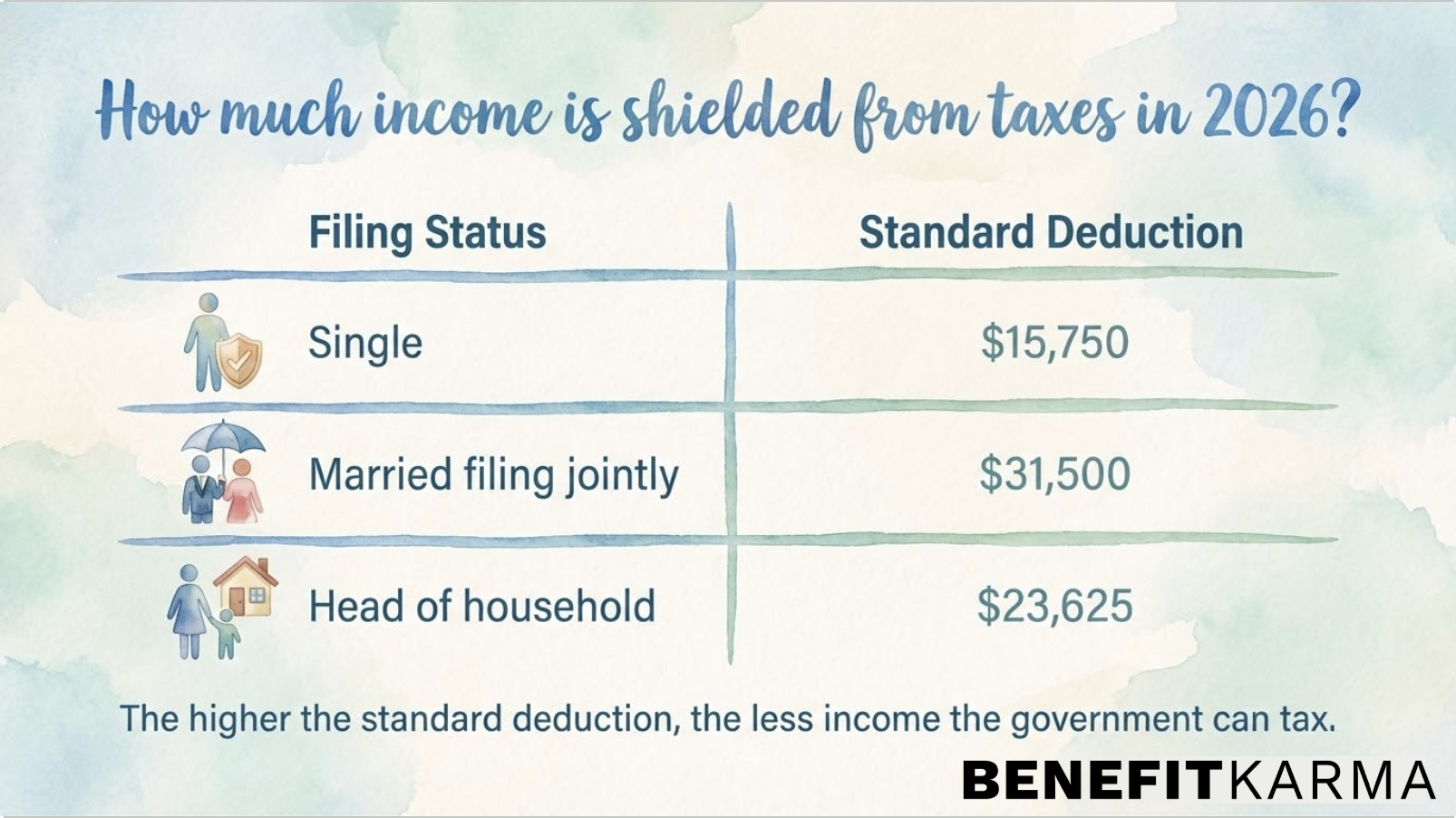

### 1. Higher standard deductions

The standard deduction reduces the amount of income the government can tax. If you take the standard deduction (instead of itemizing), your taxable income drops automatically.

For 2026 filing season, standard deduction amounts have increased:

- Single filers: $15,750

- Married filing jointly: $31,500

- Head of household: $23,625

A higher standard deduction means more income is shielded from taxes — which can increase your refund if too much was withheld from your paycheck during the year.

### 2. Expanded SALT deduction cap

The State and Local Tax (SALT) deduction cap has increased from $10,000 to $40,000 for eligible filers. This matters most for people in higher-tax states like California, New York, and New Jersey.

If you itemize and paid:

- State income taxes

- Property taxes

- Local taxes

You may now be able to deduct more than in previous years. That reduces your taxable income — which can increase your refund or lower what you owe.

### 3. New deductions for certain workers

Recent federal tax updates also introduced or expanded deductions tied to:

- Qualified tips (up to annual limits)

- Certain overtime earnings

- Eligible car loan interest

- Additional deductions for people age 65 or older

A tax deduction lowers your taxable income. Less taxable income = less tax owed.

### 4. Refundable tax credits still matter most for working families